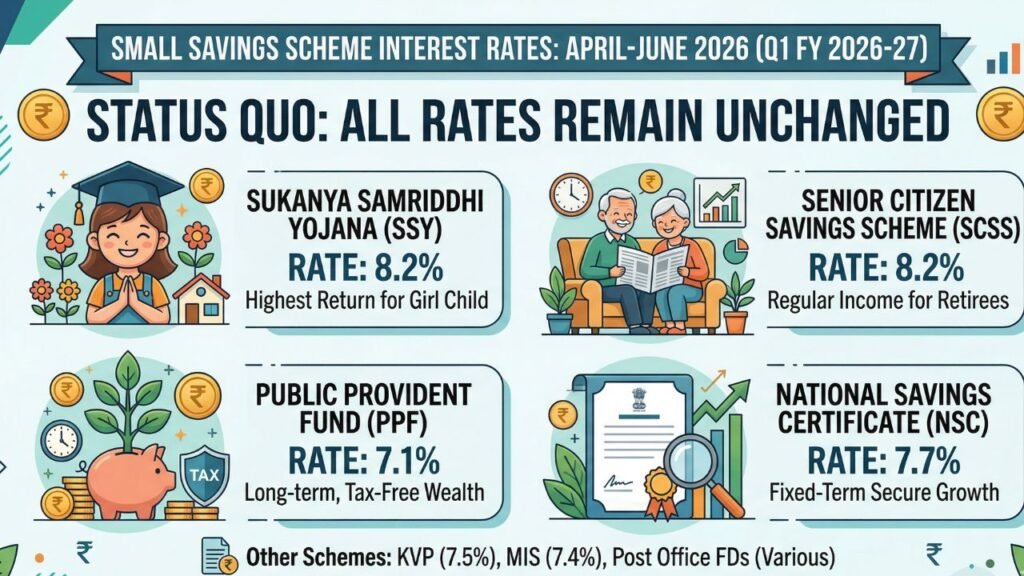

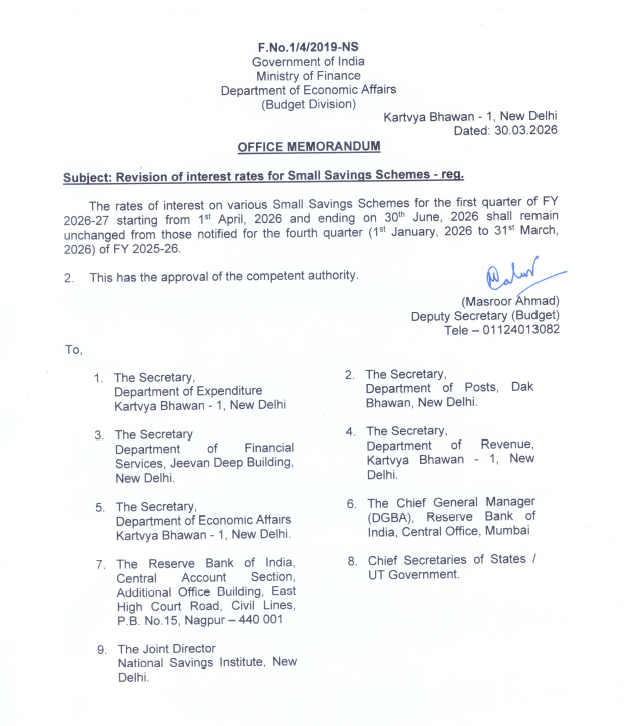

The Ministry of Finance officially announced the interest rates for small savings schemes for the first quarter of the financial year 2026-27. On March 31, 2026, the government decided to keep the interest rates unchanged. This decision affects millions of small investors, retirees, and parents across India. Investors in Public Provident Fund (PPF), Sukanya Samriddhi Yojana (SSY), and Senior Citizen Savings Scheme (SCSS) will continue to earn the same returns. This stability provides a sense of security in a fluctuating market. In this article, we explain the latest rates, the impact on your savings, and why the government chose to maintain the status quo.

Overview of Interest Rates for April-June 2026

The government reviews these rates every three months. For the April to June 2026 quarter, the rates remain identical to the January-March 2026 period. Below is the quick reference table for the current interest rates:

| Scheme Name | Interest Rate (April-June 2026) | Compounding Frequency |

| Sukanya Samriddhi Yojana (SSY) | 8.2% | Annual |

| Senior Citizen Savings Scheme (SCSS) | 8.2% | Quarterly |

| Public Provident Fund (PPF) | 7.1% | Annual |

| National Savings Certificate (NSC) | 7.7% | Annual |

| Kisan Vikas Patra (KVP) | 7.5% (Matures in 115 months) | Annual |

| Monthly Income Scheme (MIS) | 7.4% | Monthly |

| 5-Year Time Deposit | 7.5% | Quarterly |

| 3-Year Time Deposit | 7.1% | Quarterly |

| 2-Year Time Deposit | 7.0% | Quarterly |

| 1-Year Time Deposit | 6.9% | Quarterly |

| Savings Deposit | 4.0% | Annual |

1. Sukanya Samriddhi Yojana (SSY): The Highest Return

The Sukanya Samriddhi Yojana continues to offer the highest interest rate among all small savings schemes. At 8.2%, it remains a favorite for parents of girl children.

Key Highlights:

- You can open an account for a girl child below 10 years of age.

- The scheme offers excellent tax benefits under Section 80C.

- The high interest rate helps build a significant corpus for education or marriage.

- The government maintains this high rate to promote the “Beti Bachao Beti Padhao” campaign.

2. Senior Citizen Savings Scheme (SCSS): Stability for Retirees

Retirees often depend on fixed income. The Senior Citizen Savings Scheme offers a robust 8.2% interest rate. This rate remains one of the most competitive options in the debt market for seniors.

Key Highlights:

- Individuals above 60 years can invest up to ₹30 lakh.

- The scheme pays interest every quarter.

- It provides a regular income stream for elderly citizens.

- The unchanged rate ensures that retirees do not face a sudden drop in their monthly budget.

3. Public Provident Fund (PPF): The Safe Haven

The PPF interest rate stays at 7.1%. While some investors expected a hike, the PPF remains popular due to its EEE (Exempt-Exempt-Exempt) tax status.

Key Highlights:

- Investors pay no tax on the principal, the interest earned, or the maturity amount.

- The 15-year lock-in period encourages long-term disciplined saving.

- It offers complete capital safety as a government-backed scheme.

- Many experts believe 7.1% is still attractive when you consider the tax-free nature of the returns.

4. National Savings Certificate (NSC) and Kisan Vikas Patra (KVP)

The National Savings Certificate (NSC) stays at 7.7%. It is a secure investment for five years. Meanwhile, the Kisan Vikas Patra (KVP) offers 7.5%.

Key Highlights:

- KVP doubles your money in 115 months.

- NSC does not have an upper investment limit.

- Both schemes provide fixed returns without the risk of market volatility.

Why did the Government keep the Rates Unchanged?

Several economic factors influence these decisions. The Shyamala Gopinath Committee suggests that small savings rates should stay 25-100 basis points above the yields of government bonds. Currently, the Reserve Bank of India (RBI) maintains a steady repo rate. Inflation remains within the target range. Therefore, the Ministry of Finance found no immediate need to increase or decrease the rates. By keeping rates steady, the government balances the interests of savers and the cost of government borrowing.

Impact on Retail Investors

For the average household, this announcement brings a mix of relief and routine.

Positive News for Conservative Savers

If you prefer safety over high-risk stock markets, these rates are good. Banks have started lowering their Fixed Deposit (FD) rates recently. In comparison, post office schemes like SCSS and SSY offer much better returns than most 5-year bank FDs.

Impact on Tax Planning

As the new financial year (2026-27) begins in April, many people start their tax planning. Since the rates are clear, you can plan your investments in PPF and NSC early. Investing in April allows you to earn interest for the entire twelve months of the financial year.

Consistency for Goal-Based Investing

If you are saving for a child’s education or your own retirement, consistency is key. The unchanged rates mean your projected maturity amounts remain on track. You do not need to recalculate your financial goals for this quarter.

Comparing Post Office Schemes vs. Bank FDs

Many private and public sector banks offer interest rates between 6.0% and 7.5% for general citizens. Senior citizens usually get an extra 0.5%.

When we compare:

- SCSS (8.2%) is significantly higher than almost all bank FDs for seniors.

- PPF (7.1% tax-free) effectively beats a 9% taxable FD for someone in the 30% tax bracket.

- SSY (8.2%) outperforms almost every long-term debt instrument available in the market today.

- The government schemes remain the superior choice for those looking for risk-free, high-yield investments.

Official Government Links for Small Savings Schemes

| Entity / Scheme | Official Website Link |

| India Post (Department of Posts) | indiapost.gov.in |

| Ministry of Finance (DEA) | dea.gov.in/budget-division |

| National Savings Institute (NSI) | nsiindia.gov.in |

Helpline Number

| Organization / Service | Helpline Number (Toll-Free) | Timings |

| India Post Customer Care | 1800 266 6868 | 8:00 AM – 8:00 PM (Mon-Sat) |

| India Post Payments Bank (IPPB) | 155299 | 24/7 Service |

| Income Tax General Helpline | 1800 180 1961 | 9:00 AM – 6:00 PM (Mon-Sat) |

| Income Tax E-Filing Support | 1800 103 0025 | 8:00 AM – 8:00 PM (Mon-Fri) |

| Aadhar (UIDAI) Support | 1947 | 24/7 Service |

Frequently Asked Questions (FAQs)

1. Will the interest rates change in July 2026?

The government reviews the rates every quarter. The next review will happen in late June 2026. If government bond yields rise or fall significantly, the rates might change for the July-September quarter.

2. Is it the right time to invest in NSC?

Yes. Since the rate is locked at 7.7% for five years, investing now secures this return even if rates fall later this year.

3. Can I open a PPF account now to get the 7.1% rate?

Yes. You can open an account at any authorized post office or bank. The 7.1% rate applies to the current balance and all new contributions made during this quarter.

4. Why is PPF interest lower than SSY?

The government gives special preference to the girl child and senior citizens. SSY and SCSS are social welfare-linked schemes, so they offer higher incentives.

Expert Tips for Investors in Q1 2026-27

Invest Early in PPF: Deposit your PPF funds before the 5th of April. The government calculates interest on the minimum balance between the 5th and the end of the month. Doing this maximizes your yearly earnings.

- Maximize SCSS Limits: If you are a senior citizen, utilize the ₹30 lakh limit. The 8.2% rate is a “gold standard” for fixed income in the current economy.

- Diversify: Do not put all your money into one scheme. Use a mix of PPF for long-term tax-free growth and MIS or SCSS for monthly liquidity.

Monitor Inflation: While 7% to 8% looks good, always keep an eye on the inflation rate. Ensure your overall portfolio beats inflation to grow your purchasing power.

Conclusion

The Ministry of Finance’s decision to keep small savings interest rates unchanged for April-June 2026 provides much-needed predictability. In an era of global economic uncertainty, these schemes remain the backbone of the Indian middle-class savings habit. Whether you are saving for your daughter’s future through Sukanya Samriddhi Yojana or securing your own retirement through the Senior Citizen Savings Scheme, the current rates offer a lucrative and safe opportunity. Use the beginning of this new financial year to align your investments with these steady returns.